A business can still be valued when the numbers are messy. But weak management accounts create doubt, and doubt always has a price.

That matters if you’re speaking to a buyer, an investor, a lender, or HMRC. Many SMEs don’t produce clean monthly reporting, and that is more common than most owners think. The issue isn’t that a valuation becomes impossible. The issue is that it needs more judgement, better evidence, and proper accounting support.

If your records are patchy, the answer isn’t to guess. It’s to rebuild the story behind the numbers, then present it in a way that stands up to scrutiny, which is where a firm like Consult EFC adds real value.

What weak management accounts tell a buyer or investor

Management accounts are meant to do one simple job. They should show how the business is trading now, not nine months after the year end. A buyer wants to see profit trends, margins, cash movement, debtors, creditors, and whether the business is under control.

When those accounts are weak, the first question is not “what is this business worth?” It is “can I trust these figures at all?”

Poor reporting sends a signal. It suggests the owner may know the business operationally, but not financially. That does not kill a deal. It does, however, increase perceived risk. In the current UK market, that matters. As of May 2026, many traditional SMEs still sit in a broad 3 to 6 times EBITDA range, but cleaner businesses command the stronger end of that range. Messy reporting pushes value the other way.

Weak accounts don’t always reduce underlying performance. They reduce confidence in that performance.

The gaps that make numbers less reliable

The common problems are rarely dramatic. They are usually small gaps that build up.

Late reports are one issue. If monthly accounts arrive six or eight weeks late, they stop being management tools and become historical paperwork. Missing accruals are another. If costs are recorded only when paid, monthly profit swings become hard to interpret.

Owner expenses often blur the picture. Personal travel, family mobile contracts, non-trading meals, or a car that is half business and half lifestyle, these all distort true earnings. One-off costs can do the same if they are left sitting in normal trading results. Legal fees from a dispute, restructuring costs, or a major repair bill may be real cash costs, but they are not always ongoing business costs.

Then there is the tie-back problem. If the monthly figures do not reconcile to the statutory accounts, buyers start asking which set is right. Add weak cash flow tracking, unclear debtor balances, or stock numbers that no one fully trusts, and the valuation becomes less about maths and more about risk control.

Each gap affects the process differently. Some reduce profit quality. Some weaken the balance sheet. Some make forecasting harder. Taken together, they widen the valuation range and lower confidence in the top end.

How weak reporting affects trust and deal value

Real buyers do not pay premium multiples for numbers they cannot test. They either reduce the multiple, narrow the valuation range, or shift more of the price into a later earn-out.

That is how risk gets priced in practice. Not with theory, with deal terms.

If due diligence turns into a forensic rebuild of the accounts, the buyer’s costs rise. Their timeline stretches. Their confidence falls. A lender may take a stricter view. An investor may ask for stronger downside protection. HMRC may want more support for any assumptions used in a share valuation.

This is why weak management accounts often lead to more questions, more negotiation, and a lower headline figure. Sometimes the business itself is solid. Sometimes the reporting simply fails to prove it.

A credible valuation in this situation needs two things. First, the numbers must be normalised. Second, the explanation behind them must be clear. That is where experienced judgement matters more than a template.

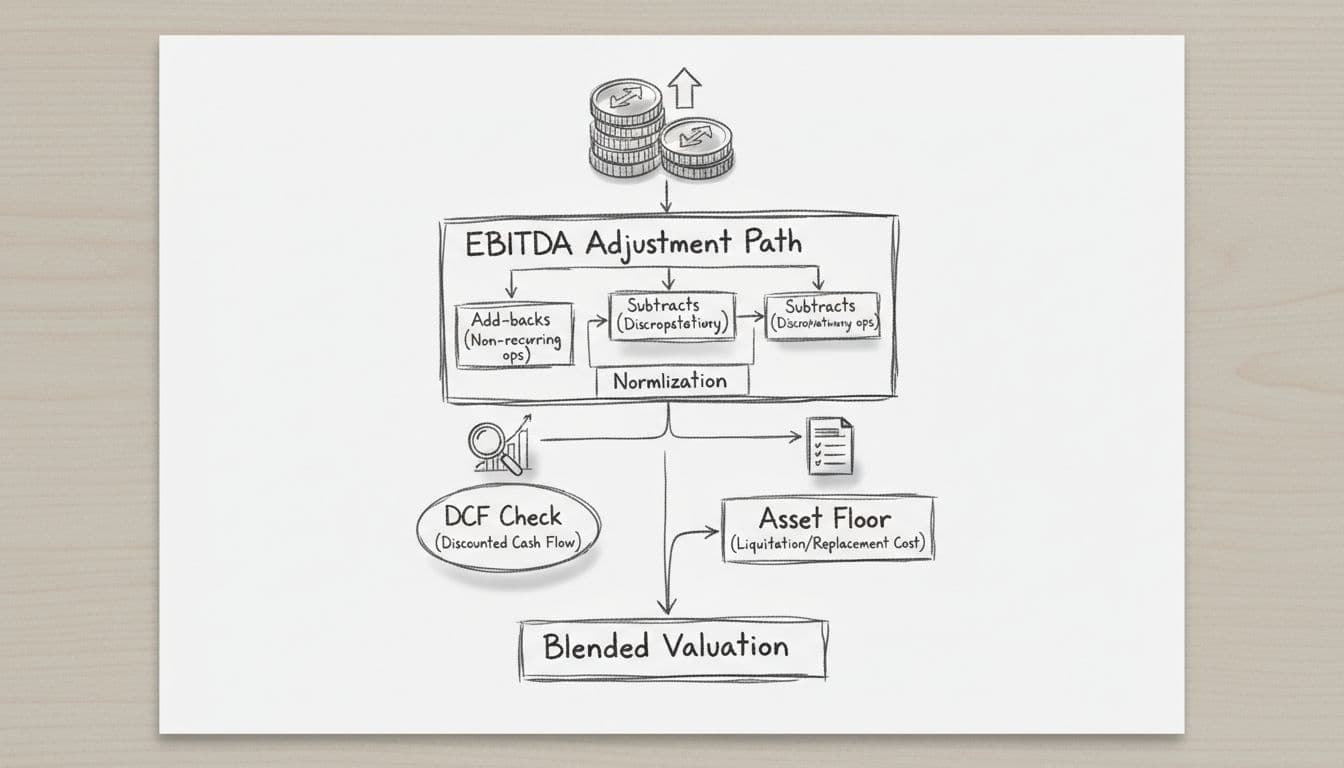

Which Business Valuation Methods Work Best With Weak Financial Records?

When the accounts are imperfect, no single formula does all the work. The best valuations usually blend methods, then weigh them according to the quality of the evidence.

For most UK SMEs, the practical starting point is adjusted EBITDA. A discounted cash flow model can then act as a cross-check, if the forecast is credible. Asset value often provides a floor where earnings cannot be relied on. That mix is not academic. It is how sensible valuations are built when the reporting is less than perfect.

Calculating Adjusted EBITDA to Find True Maintainable Earnings

Adjusted EBITDA is usually the most useful method for SMEs with weak accounts because it focuses on maintainable earnings. In plain English, it asks: what would this business earn for a normal owner, after removing the noise?

Common add-backs include personal expenses through the company, one-off legal bills, unusual restructuring costs, and owner pay that is far above or below market rate. If the business paid the owner £20,000 but would need to pay a replacement managing director £80,000, that matters. If the owner ran personal holidays through the company, that matters too.

The point is not to inflate profit. The point is to show the true trading performance of the business. Done properly, this creates a more defensible EBITDA figure for valuation purposes.

For many SMEs, this is the method that gives the clearest answer. It is practical, it reflects how buyers think, and it can be supported with evidence even where the monthly reporting is weak.

When discounted cash flow helps, and when it misleads

DCF has its place. If the business has a realistic forecast, solid customer relationships, and a clear route to cash generation, it can be useful. But weak accounts make DCF dangerous when used badly.

Why? Because the model can look precise whilst resting on weak assumptions. A spreadsheet can produce a neat answer down to the pound. That does not make it reliable.

If the historic numbers are patchy, forecast cash flow must be conservative and evidence-based. Orders on hand, contracts, visible pipeline, known staffing costs, and working capital needs all matter. If those supports are missing, DCF should not carry the valuation on its own. It should act as a sense-check against the earnings approach, not a substitute for proof.

Why asset value sometimes becomes the floor

Where profit data cannot be trusted, asset-based valuation becomes more important. This method looks at the fair value of assets less liabilities. It is often helpful for asset-heavy businesses, companies with machinery or property, or cases where earnings are volatile and unclear.

It can also help where a buyer wants comfort that there is a base level of value even if trading underperforms.

That said, asset value usually understates a going concern. It may capture stock, plant, debtors, or property, but it may miss the real worth of customer relationships, trained staff, and repeat earnings. So it is best seen as a floor, not the whole story.

How to clean up the numbers before you value the business

The quality of your valuation is tied to the quality of the inputs. Better accounts do not always mean a dramatically higher value, but they nearly always produce a more credible one.

If you are preparing for a sale, fundraising round, shareholder dispute, EMI process, or HMRC review, clean-up work before the valuation is time well spent. It reduces challenge points later and gives your adviser more solid ground to work from.

Separate personal spending and one-off items from trading performance

Start with normalisation. Go through the accounts and identify items that are not part of ordinary trading.

This includes personal expenses, above-market or below-market owner salary, family costs through the business, private travel, and unusual non-recurring items. A one-off legal fee should not depress maintainable earnings if it is not expected to repeat. Equally, an unusual spike in revenue should not be treated as permanent if it was a single event.

The aim is clarity. Buyers do not expect perfection. They do expect honesty and support for every adjustment.

Make sure monthly management accounts tie back to statutory accounts

Reconciliations matter more than most owners realise. If monthly accounts can be tied back to the year-end accounts, and key balances are supported, trust rises quickly.

That means using a consistent format each month. It means reconciling bank, VAT, payroll, debtors, creditors, and stock where relevant. It means being able to explain why monthly profit differs from cash in the bank.

A tidy reconciliation pack can save a deal from drifting into unnecessary doubt. It shows control. It shows discipline. Most of all, it shows that the numbers are not being moved around to fit a story.

Build a realistic forecast based on evidence, not hope

A 12 to 24 month forecast is often enough. It does not need to be elaborate. It does need to make commercial sense.

Base it on current customers, signed contracts, repeat order patterns, open pipeline, expected staff costs, rent, finance commitments, and tax. If margins are tightening, show that. If one customer may leave, account for it. Optimism without support damages trust faster than a cautious forecast ever will.

This is where Consult EFC can make a real difference. A forecast prepared with accounting discipline carries more weight than a sales-led spreadsheet with no link to history.

Common mistakes that can damage the valuation

Weak-account valuations often go wrong in predictable ways. Most of them come from trying to force a strong result out of weak evidence.

That approach rarely survives scrutiny.

Using a strong multiple on weak data

Owners often look at headline sector multiples and assume those numbers apply to them. They may not.

A business with clean reporting, recurring income, low customer concentration, and strong systems can justify a better multiple. A business with weak accounts, poor visibility, and heavy owner reliance cannot expect the same treatment.

If a comparable business might attract 5 times EBITDA, weak reporting may push that down to 3 or 3.5 times. That is not unfair. It is how risk is priced.

Treating DCF as if it is more certain than it really is

This is a common error in SME valuations. The spreadsheet looks polished, the discount rate looks technical, and the answer feels precise. But poor inputs still produce poor outputs.

If historical reporting is weak, every forecast assumption deserves challenge. Revenue growth, gross margin, staff cost inflation, debtor days, capital spend, all of it. A DCF can support the valuation, but it should not create false confidence.

Forgetting that buyers price in risk

A buyer is not only buying earnings. They are buying proof, control, and transferability.

Where the accounts are weak, buyers often respond through structure. They may ask for deferred consideration, warranties, indemnities, or an earn-out. Sometimes the headline price stays close to expectation, but more of the value is pushed into future performance conditions.

That is still a lower-value deal in economic terms. Cash later is not the same as cash now, especially when it depends on post-completion performance.

Conclusion

Weak management accounts do not stop a business being valued. They do mean the valuation must be built with more care, stronger evidence, and more professional judgement.

The strongest answer usually comes from normalised earnings, sensible method selection, and clear support for every adjustment. When that work is done properly, messy reporting can still be turned into a credible valuation story.

If you want a figure that stands up to buyer scrutiny, investor challenge, or HMRC review, the quality of the process matters as much as the number itself. That is exactly where Consult EFC helps SMEs grow, raise money, and exit on better terms.

Not sure what your business is worth right now?

Request a confidential valuation — ICAEW Chartered Accountants, Big Four trained. No junior analysts. Fixed fees.

Request My Valuation

Over 12 years across Big Four audit, Investment Banking and corporate advisory. Kishen works with UK SMEs on valuations, exit planning, fundraising and financial strategy. ICAEW regulated. Big Four trained. Based in London.