Choosing between EMI options and growth shares sounds like a tax question. It isn’t only that. It’s also about size, stage, investor plans, control, and what sort of reward structure your team will understand and trust.

For many UK SMEs, both routes can work. They simply work in different ways. Since the EMI rules widened from 6 April 2026, more scaling companies can now use EMI than before, which makes the choice more interesting, not less.

If you’re a founder, finance lead, or director trying to make a sensible decision, start with the mechanics first. The tax only makes sense once the structure does.

How EMI schemes and growth shares work in plain English

At a simple level, EMI and growth shares are both ways to reward key people with equity-linked upside. After that, the similarity starts to fall away.

What an EMI option really gives an employee

An EMI option is not a share on day one. It’s a right to buy shares later, usually at a price fixed when the option is granted. That matters. The employee doesn’t need to put cash in upfront, and they don’t become a shareholder immediately.

In practice, options often vest over time or become exercisable on an exit. If the company grows, the employee can buy at the earlier agreed price and sell at a higher value. That’s where the reward comes from.

For qualifying UK companies, EMI is popular for a reason. If it’s set up properly, the tax treatment is often strong. In many cases there is no income tax on grant, and no income tax on exercise if the exercise price is at least the market value agreed at grant. Future growth is then usually taxed under capital gains rules on sale, not as salary.

That combination, low upfront cost, familiar structure, and attractive tax treatment, is why EMI is often the first option for senior hires and core team members.

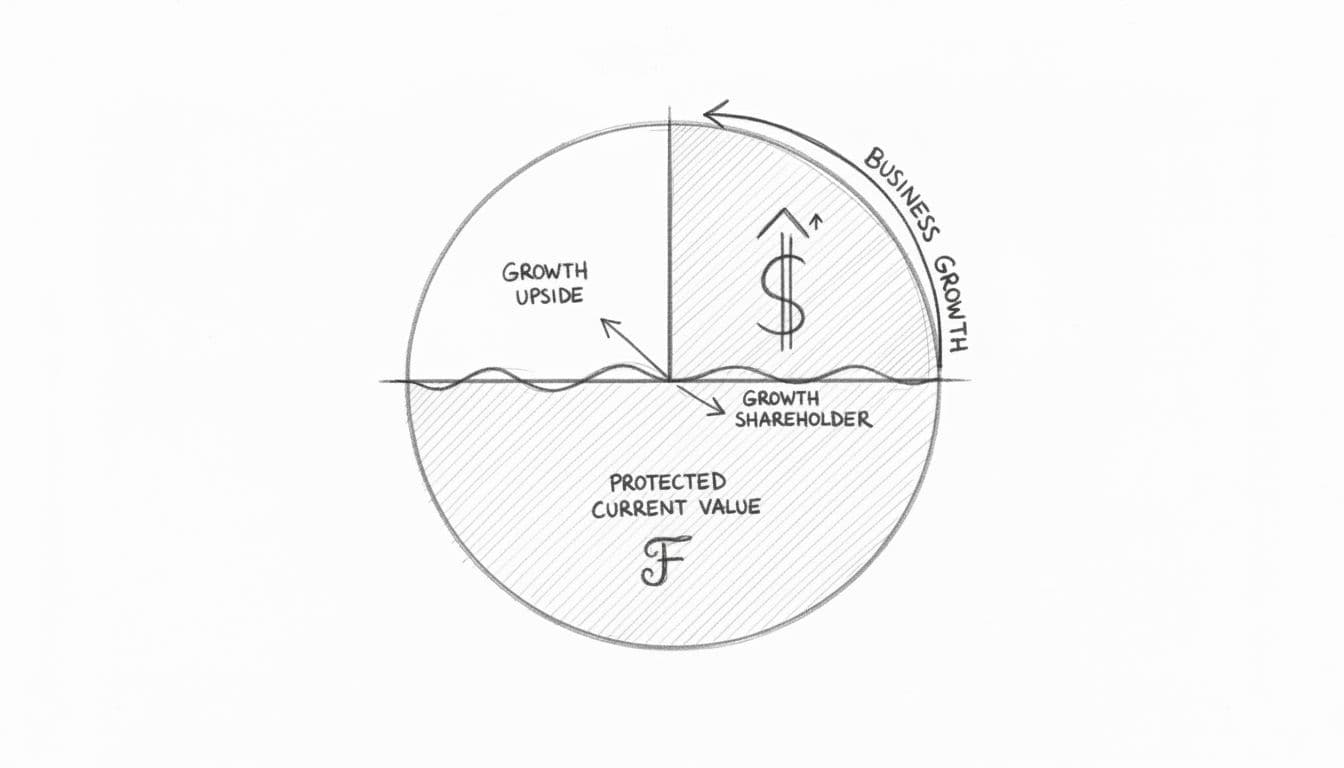

How growth shares reward people only on future upside

Growth shares are real shares from the start, but they are designed to participate only in value created above a hurdle. Think of the hurdle as a fence around today’s value.

Say your business is worth £5 million today. You issue growth shares with a £5 million hurdle. If the company later sells for £8 million, the growth shares only share in the £3 million above that line. Existing founders and investors keep the value already built.

This is why growth shares appeal to founder-led businesses. They can reward future contribution without handing away current value. The recipient becomes a shareholder, though often with limited rights and carefully drafted restrictions.

That sounds neat, but the design work matters. If the hurdle, rights, or tax analysis are weak, the structure can create problems later, especially under due diligence.

Key Differences: Tax, Control, and Setup for UK SMEs

The real choice is not theory. It’s what happens to tax, control, legal work, timing, and founder protection.

This comparison keeps it practical:

| Factor | EMI option | Growth shares |

|---|---|---|

| What the person gets | A right to buy shares later | Shares immediately |

| Upfront cost for staff | Usually low or nil at grant | Often low market value, but still a share issue |

| Tax position | Often more efficient if rules are met | Can be efficient, but more dependent on drafting and valuation |

| Control impact | No shareholder rights until exercise | Shareholder exists from issue date, even if rights are limited |

| Setup style | More standardised | More bespoke |

| Best fit | Qualifying SMEs hiring employees | Companies needing flexibility or protection of current value |

The broad takeaway is simple. EMI is usually cleaner. Growth shares are usually more tailored.

Tax treatment and who keeps more at exit

For employees, EMI often wins on simplicity and outcome. If the option is granted at a proper market value and the rules are followed, more of the gain may fall into capital treatment rather than income tax and NIC. That can make a material difference at exit.

Growth shares can still work well from a tax angle, but the margin for error is smaller. The valuation at issue, the hurdle design, any restrictions, and the paperwork all need to stack up. If they don’t, HMRC may take a different view, and the person you meant to reward keeps less than expected.

If the tax result depends on a weak valuation or vague drafting, it is not a strong incentive plan.

Cost, legal work, and how long setup takes

EMI still needs work. You’ll want a proper share valuation, option documents, board approvals, scheme registration, and annual reporting to HMRC. But the market knows the shape of EMI. Lawyers, accountants, investors, and senior hires have usually seen it before.

Growth shares tend to need more bespoke legal input. You are often creating a new share class, amending articles, aligning the shareholders’ agreement, setting the hurdle, and drafting leaver and transfer provisions. None of that is impossible. It is more custom work.

Control, dilution, and founder protection

With EMI, the employee is not a shareholder until exercise. That means no voting rights, dividend rights, or immediate cap table movement in the same way. For many SMEs, that feels cleaner.

Growth shares create a shareholder from day one. Rights can be heavily limited, but the person is still in the structure. That matters if founders want tight control or a simple cap table before funding.

On the other hand, growth shares can protect existing value more precisely. If founders want incentives tied only to future growth, they can be the better tool.

When EMI Options Are the Strongest Choice

For many qualifying UK SMEs, EMI is still the starting point. Not because it’s fashionable. Because it often gives the best mix of tax efficiency, staff appeal, and administrative clarity.

Taking Advantage of the April 2026 EMI Rule Changes

From 6 April 2026, EMI became available to more businesses. The main limits are now broader: fewer than 500 full-time equivalent employees, up to £120 million of gross assets, and a total unexercised EMI options pool of up to £6 million. The maximum exercise window is also now 15 years.

Those changes matter for scale-ups that previously fell outside the rules too early. If your company still carries on a qualifying trade, has a UK permanent establishment, remains independent, and your option holders meet the working time and shareholding tests, EMI is often the first route to examine.

There is one caution. Some “specified companies” remain under the old size limits. So eligibility still needs checking, not assuming.

Best for hiring and retaining key staff with strong tax incentives

When cash is tight, equity has to do real work. EMI often does. Senior hires usually understand the idea quickly: stay, help build value, and share in the upside on a tax-efficient basis.

That matters when you’re competing with larger employers on salary. A structure people can understand in one meeting is better than one that needs three follow-up calls and a tax memo.

Best for businesses wanting HMRC-backed valuation comfort

One of EMI’s strongest features is valuation comfort. In many cases, the market value for option grant can be agreed with HMRC in advance. That reduces the risk of getting the strike price wrong.

For founders planning a raise or an exit, that matters. A poorly supported grant price can become a due diligence issue later. A defensible valuation gives the board, employees, and future buyers more confidence.

When Growth Shares Make More Sense for Founders

Growth shares are not second best. They are often the right answer when EMI is unavailable or too narrow for what the business needs.

Useful for companies that no longer fit EMI rules

Some businesses have outgrown EMI. Others fail the trade conditions, group structure rules, or independence tests. In those cases, growth shares often become the practical alternative.

This is common in more mature scale-ups, asset-heavy companies, and businesses with more complex ownership structures. If EMI is off the table, growth shares can still create a credible equity story.

Helpful when you want to reward contractors or other non-employees

EMI is for employees. That boundary matters. If you want to reward consultants, advisers, or other non-employees, growth shares can offer more flexibility.

That does not mean they are casual to issue. It means the structure can be built around a wider group of contributors, provided the legal and tax work is done properly.

Better when founders want to protect present value and keep incentives tied to growth

This is where growth shares often stand out. Founders may be happy to reward future success, but not to dilute value already created before the recipient joined.

A hurdle solves that problem. It can ring-fence today’s equity value for existing shareholders and only open participation above that line. For businesses with investor money already in, or a meaningful valuation today, that can be the cleanest commercial answer.

Valuation and Compliance: Mistakes to Avoid

Both routes depend on valuation. Both can fall over if the paperwork is weak. The difference is where the pressure points sit.

Why a robust share valuation matters before you issue anything

If the value is wrong at the start, the tax position can be wrong at the end. That’s true for EMI and growth shares alike.

An over-optimistic or under-supported valuation can create income tax exposure, employee disputes, and awkward questions in a funding round or sale. Buyers and investors will look at how the equity plan was set up. If the valuation file is thin, that becomes your problem later.

Need HMRC Valuation Comfort? Don’t let a weak share valuation trigger unexpected income tax for your key hires. Our ICAEW-regulated team builds defensible valuation files designed to withstand HMRC scrutiny. Contact us today.

What HMRC expects from EMI valuations

With EMI, the basics are clear. Get the share valuation right before grant, register the scheme correctly, file annual employment-related securities returns, and keep a full record set. That includes valuation support, board minutes, grant documents, and evidence that the employee met the working time tests.

Many SMEs treat this as admin. It isn’t. It is the foundation for keeping the intended tax treatment intact.

What growth share drafting must cover to avoid problems later

Growth shares need sharper drafting. The hurdle must be clear. The rights must be clear. Leaver terms, transfer limits, dividend rights, voting rights, and sale mechanics must all line up.

If they don’t, you can end up with tax risk, shareholder tension, or confusion at exit, which is the worst time to discover that the paperwork says less than everyone thought it did.

For businesses that expect investor or buyer scrutiny, this is where a proper valuation and carefully structured documentation pay for themselves.

Final thoughts

If your company qualifies, EMI is usually the first place to look. It is familiar, often tax-efficient, and easier to explain to the people you are trying to recruit and keep.

Growth shares come into their own when EMI does not fit, when flexibility matters more, or when founders want to protect today’s value and only reward future upside. Different tool. Different job.

Ready to structure your equity properly? A proper review can save time, protect value, and stop expensive mistakes before they get baked into your cap table. Contact Consult EFC in confidence today

Not sure what your business is worth right now?

Request a confidential valuation — ICAEW Chartered Accountants, Big Four trained. No junior analysts. Fixed fees.

Request My Valuation

Over 12 years across Big Four audit, Investment Banking and corporate advisory. Kishen works with UK SMEs on valuations, exit planning, fundraising and financial strategy. ICAEW regulated. Big Four trained. Based in London.