A delayed EMI scheme often starts with something small, not something complex. One missed date, one wrong assumption, one document that doesn’t match the rest.

That matters more than most founders expect. If you’re using EMI to reward key staff, support fundraising, or get exit-ready, admin mistakes can hold up tax clearances, create buyer questions, and put the scheme’s tax advantages under pressure.

The good news is simple: most delays are avoidable if you get the foundations right early.

Get the basics right before you submit anything to HMRC

Many EMI problems start before the first filing. The scheme may sound right in principle, but HMRC looks at eligibility, terms, timing, and records. If those basics are off, the back-and-forth starts.

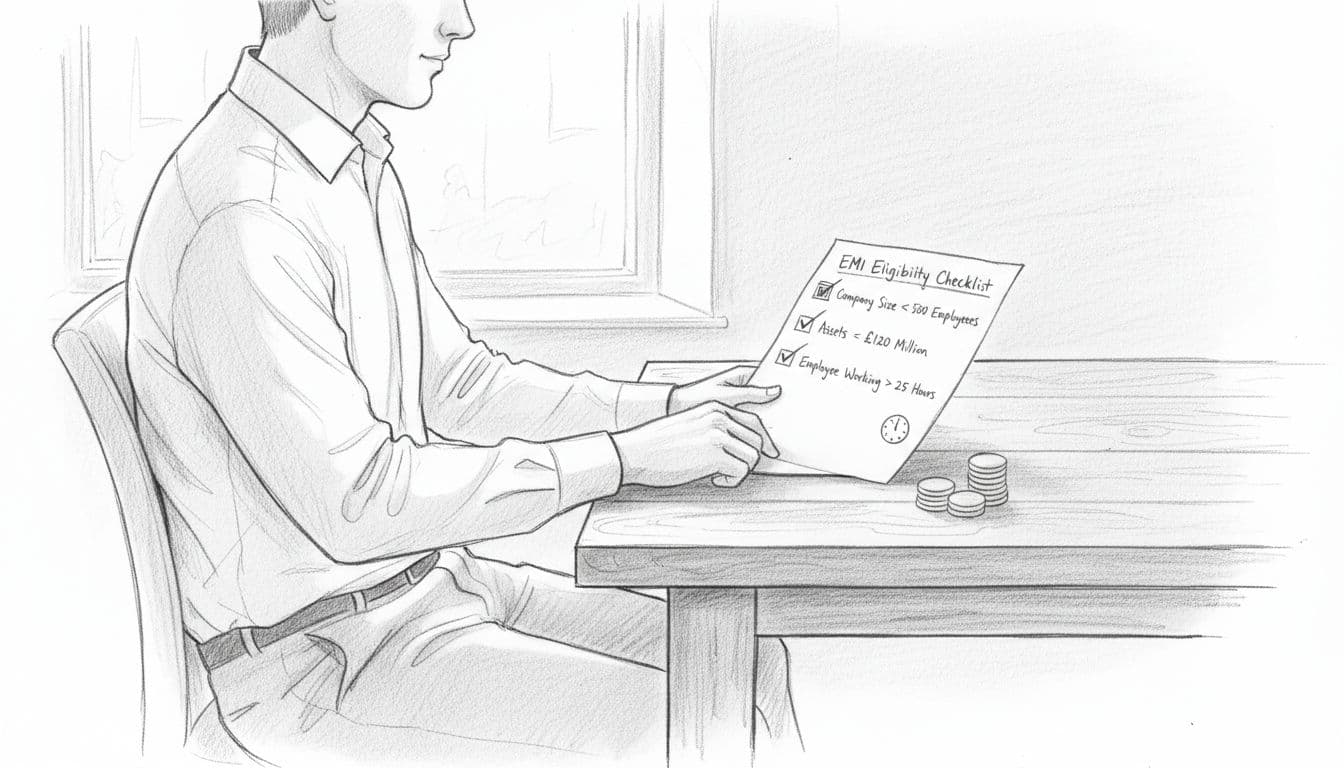

Check the company and employee eligibility rules first

Start with the hard rules. As at May 2026, the company must usually have fewer than 500 full-time equivalent employees, gross assets of no more than £120 million, and a UK permanent establishment. There is also a limit on the total value of shares under EMI options, currently £6 million.

Then look at the employee. They must be a genuine employee, not a name on paper. Working time matters. So does their role. So does their existing shareholding. If someone holds more than 30% of the company, EMI is usually off the table.

One wrong assumption here can slow everything down. Worse, it can mean options were never qualifying in the first place.

Make sure the scheme terms match the company’s wider documents

EMI paperwork doesn’t sit on its own. The option agreement, plan rules, articles of association, shareholder agreement, and board approvals all need to say the same thing in practical terms.

This is where trouble creeps in. You might have vesting in the option letter that doesn’t match the articles. Or an exercise trigger that conflicts with leaver provisions. Or board minutes approving terms that were later changed informally.

That may not show up on day one. It often shows up during HMRC queries, investment due diligence, or a sale. By then, fixing it is slower, more expensive, and far less comfortable.

EMI should read like one joined-up process, not five documents written by different people on different days.

The most common HMRC filing mistakes that slow approval

This is where most delays come from. Not strategy. Not intent. Paperwork, timing, and record keeping.

Missing the reporting deadline for option grants

At the time of writing, EMI option grants still need to be notified to HMRC within 92 days of grant. That remains the position in May 2026, even though the grant notification requirement is due to fall away from April 2027.

Miss that 92-day window and you risk more than delay. You may lose key tax advantages attached to the option.

The fix is boring, but it works. File as soon as the grant is made. Put the deadline in the diary on the same day. Make one person responsible. Not shared responsibility. Named responsibility.

Using the wrong valuation, or leaving it too late

A weak valuation can slow the process before it starts. So can a valuation that was agreed, then left sitting until the commercial facts changed.

The exercise price needs to be supported properly. If HMRC sees a number with thin logic behind it, questions follow. If the valuation is stale, questions follow again. That is not what you want when you’re trying to move quickly around a funding round or senior hire.

Get the valuation agreed in good time, then grant options while that valuation is still current. If the business has changed materially, re-check it. A proper HMRC-focused valuation is not admin for admin’s sake. It’s part of protecting the scheme.

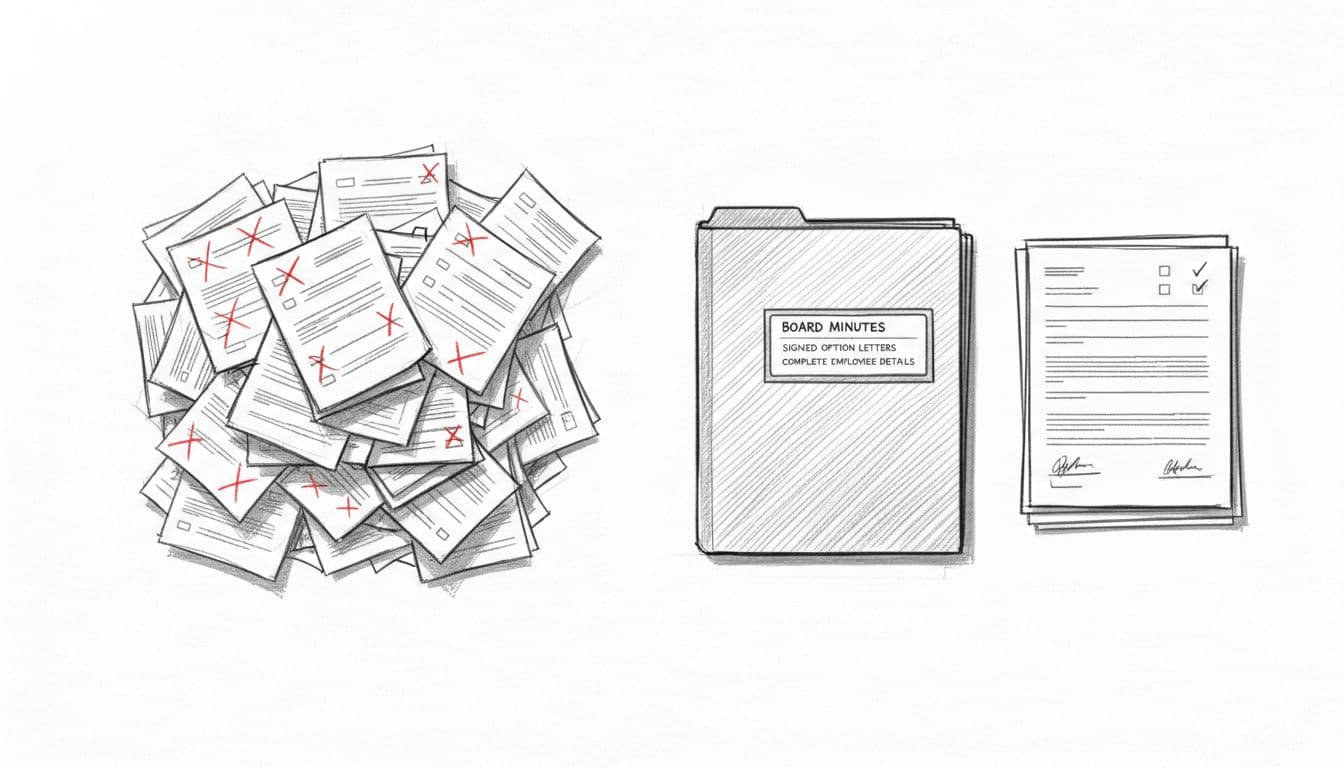

Submitting incomplete or inconsistent paperwork

This one is common, and avoidable. Missing board minutes. Unsigned option letters. Wrong grant dates. Employee details missing. Share numbers that don’t match across the cap table, valuation paper, and grant documents.

HMRC, investors, and buyers all look for the same thing: a clear audit trail. If the story changes from one document to the next, confidence drops fast.

Tidy records save time later. They also reduce the chance of awkward clean-up work during due diligence.

Forgetting the annual EMI return and scheme updates

EMI isn’t a one-off event. The annual return still matters. In the UK, EMI returns are due by 6 July following the end of the tax year.

Companies get caught out because the initial grant felt like the main task. Then a year passes. Someone leaves. A grant lapses. Terms change. No one updates the records properly.

That creates risk on two fronts. First, compliance slips. Second, your internal position stops matching what HMRC expects to see if questions arise later.

How to avoid delays by managing changes after the grant

Even well-set-up EMI schemes can run into problems once the business starts moving quickly. Growth is good. Casual admin around growth is not.

Watch for changes that can break EMI status

The biggest risk is assuming the original position stays true. It doesn’t always. An employee may change role, reduce hours, or stop meeting the working time test. The company may outgrow key limits. A corporate transaction may alter the facts around the option.

These are the moments that need review. Fast-growing SMEs and start-ups are most exposed because things change quickly and the scheme is rarely top of the weekly priority list.

The answer isn’t panic. It’s monitoring. Put review points around promotions, leavers, restructures, and funding events.

Avoid casual changes to option terms once they are granted

Post-grant amendments need care. Extending exercise periods, changing vesting, or softening leaver terms can all have tax or compliance effects if handled badly.

The common mistake is treating EMI like a normal HR document. It isn’t. Once granted, the terms have tax consequences.

Review any amendment before it is agreed. Not after. That one habit avoids a lot of delay, and a lot of uncomfortable explanations later.

A simple process that helps SMEs get EMI approval faster

Most EMI schemes don’t need more complexity. They need a cleaner process.

Build one clear approval pack before you file

Pull everything into one place before submission. Eligibility checks. Valuation support. Signed option documents. Board minutes. Cap table support. Any shareholder approvals.

That pack does two jobs. It makes HMRC review easier, and it makes later due diligence far easier too.

Use a named owner and a deadline calendar for every grant

EMI admin often fails because it sits between finance, legal, and management. No one owns it fully. That is where dates get missed.

Give one person, or one lead adviser at Consult EFC, responsibility for the grant timetable, reporting dates, and review points. For SMEs juggling hiring, fundraising, and exit planning, that single line of ownership makes a real difference.

Final thoughts

Most EMI delays come from avoidable mistakes, not from the scheme itself. Get the eligibility right, get the paperwork right, get the timing right, and keep watching the scheme after grant.

That is the real protection. Not guesswork. Not patching things later. Control from the start.

Consult EFC helps SMEs take that careful, human, growth-focused approach, so the tax advantages are protected and the business stays ready for investor scrutiny, buyer diligence, and the next stage of growth.

Not sure what your business is worth right now?

Request a confidential valuation — ICAEW Chartered Accountants, Big Four trained. No junior analysts. Fixed fees.

Request My Valuation

Over 12 years across Big Four audit, Investment Banking and corporate advisory. Kishen works with UK SMEs on valuations, exit planning, fundraising and financial strategy. ICAEW regulated. Big Four trained. Based in London.