When shareholders fall out, the price of the shares becomes the fight. It affects buyouts, settlements, court claims, and who keeps control of the business.

A proper business valuation for shareholder disputes is not just about the numbers. It’s about fairness, evidence, and protecting the company from further damage while the dispute is still active.

For UK SMEs, that means getting a clear, defensible figure that can stand up to scrutiny and help move the matter forward. Consult EFC handles this work with an independent, partner-led approach, so you get a valuation that is built for real-world decisions, not guesswork.

What makes shareholder dispute valuations different from a normal business valuation?

A shareholder dispute valuation is not a standard pricing exercise. The numbers may look familiar, but the question is different, the evidence is sharper, and the stakes are often personal as well as financial.

In a normal business valuation, the focus is often on what a willing buyer would pay in the open market. In a dispute, the issue is usually fair value, the conduct of the parties, and the point at which the relationship broke down. That changes the whole job.

Why the reason for the dispute changes the value

The cause of the dispute matters because it changes what is being valued and how the figures should be adjusted. If a shareholder has been excluded from management, denied information, or cut off from dividends, the valuation cannot ignore that reality and pretend the company is operating normally.

Poor conduct also leaves a mark. If one side has diverted business away, taken excessive drawings, or damaged the company through bad decisions, the valuation may need to strip out those effects or adjust for them. That is why a dispute valuation is rarely neat and tidy. It has to reflect the real business, not the textbook version.

Common dispute triggers often affect valuation in different ways:

- Exclusion from management can change earnings assumptions, especially where the business depended on the excluded shareholder.

- Unpaid dividends may point to a wider squeeze-out strategy, which affects settlement discussions and fairness arguments.

- Broken trust can expose weak records, related-party transactions, or informal decision-making.

- Poor conduct may reduce maintainable earnings or require one-off adjustments to normalise the numbers.

The key point is simple. A proper valuation is not just about applying a multiple and moving on. It is about understanding what happened, when it happened, and how that history has affected value.

A shareholder dispute valuation has to follow the facts on the ground, not the polished story the business might tell in ordinary trading conditions.

Why courts and lawyers care about fair value

In shareholder disputes, fair value is the phrase that matters. In plain English, it means a price that reflects what the shares are really worth in the circumstances, without rewarding bad behaviour or distorting the result with crude market assumptions.

That is why courts usually expect an evidence-based report. They want a valuation that is grounded in accounts, trading history, industry evidence, and proper assumptions. They do not want guesswork dressed up as precision.

This is also why minority shareholders are not automatically discounted in forced buyouts. In a normal market sale, a small stake may attract a discount because it carries less control and is harder to sell. In a dispute, that approach can produce an unfair result, especially where the majority’s conduct caused the breakdown.

A strong report helps both sides because it gives the dispute something concrete to work with. It can narrow the gap, expose weak assumptions, and make settlement more realistic. Without that, the parties often argue about principle long before they ever reach price.

For practitioners, that means the valuation needs to be:

- Independent, so neither side can dismiss it as spin.

- Defensible, so the assumptions can stand up to challenge.

- Practical, so it helps move the case towards a resolution.

That is the difference. A normal business valuation asks, “What is the business worth?” A shareholder dispute valuation asks, “What is fair, on these facts, for these shares, at this point in the fight?”

The main valuation methods used in UK shareholder disputes

There is no single formula that fits every shareholder dispute. The right method depends on the shape of the business, the quality of the records, and what is actually in dispute.

For UK SMEs, the aim is usually to reach a fair, defensible figure that reflects the company as it really is, not as one side would like it to be. That means testing more than one approach, then using the one that best matches the facts.

Earnings-based valuation for profitable SMEs

For a trading business with steady profits, the starting point is often maintainable earnings or EBITDA. In plain terms, you strip out anything unusual, one-off, or personal to the owner, then work out what the business is really capable of earning year after year.

That means adjusting the accounts first. You might add back non-recurring costs, remove excess director pay, or normalise private expenses run through the company. Once those profits are cleaned up, they are multiplied by an appropriate earnings multiple to give a valuation.

The formula is simple:

Maintainable earnings x multiple = business value

The challenge is getting both parts right. A higher multiple suits a stable business with recurring income, strong margins, and low customer concentration. A lower multiple is more common where the owner is heavily involved, the contracts are short-term, or the business depends on a small number of clients.

For many profitable SMEs, this is the most useful method because it reflects the business’s actual trading power, not just what sits in the bank at year-end.

This method is especially common where the dispute is about an ongoing business, not a distressed one. It gives both sides a commercial starting point, and it is easier to explain to a judge, solicitor, or opposing expert than a more theoretical model.

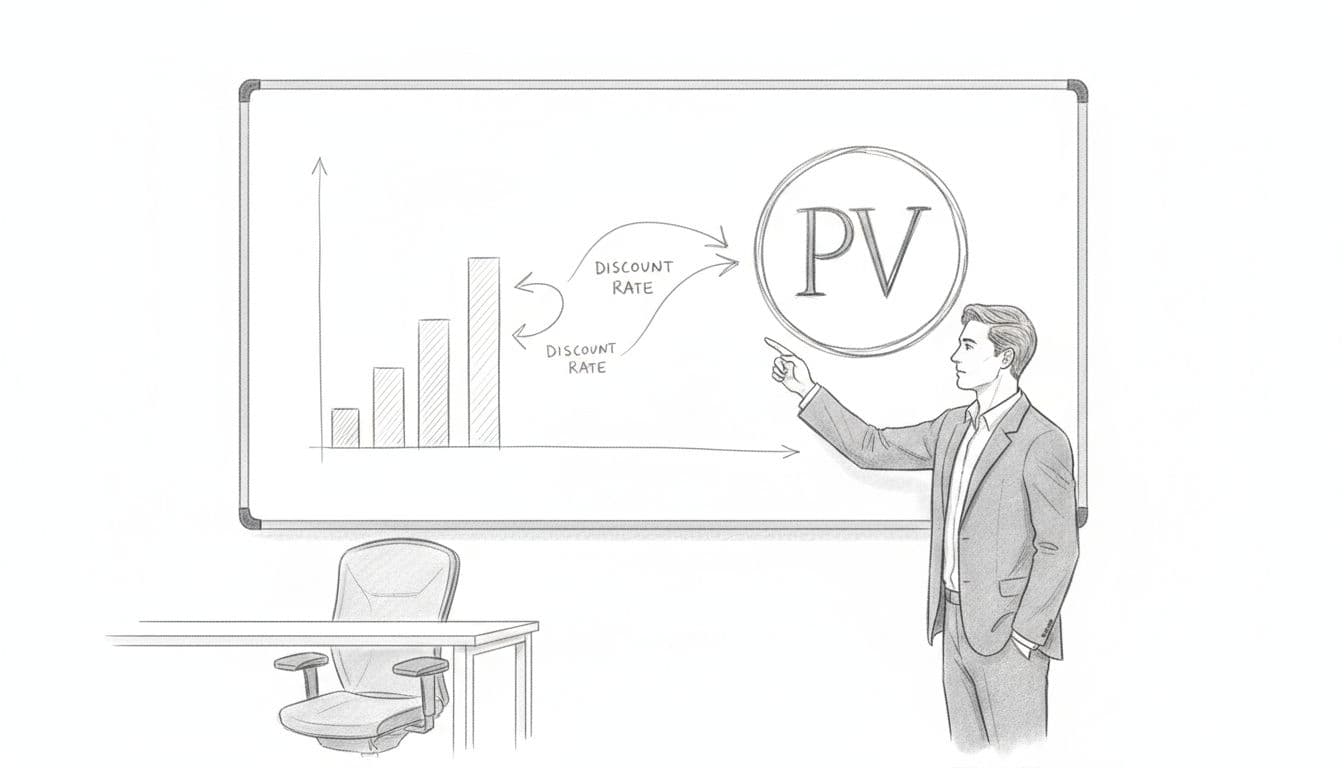

Discounted cash flow when future performance matters

Discounted cash flow, usually called DCF, looks at the cash the business is expected to generate in the future, then converts that into today’s value. It is a forward-looking method, so it works well when the future matters more than the past.

That makes it useful where the business has visible growth, long-term contracts, or changing margins. A recent contract win, a new product line, or a planned squeeze on costs can all justify a DCF approach when earnings alone would miss the point.

The process is straightforward, at least on paper:

- Forecast the expected cash flows over a set period.

- Apply a discount rate to reflect risk and the time value of money.

- Add a terminal value if the business is expected to continue beyond the forecast period.

The assumptions matter a great deal. Small changes to growth rates, margins, or the discount rate can move the result sharply. That is why DCF only works properly when the forecasts are realistic and backed by evidence, not optimism.

If the assumptions are stretched, the result becomes fragile. In a dispute, that is a problem. The other side will test every line, and a weak model can collapse fast.

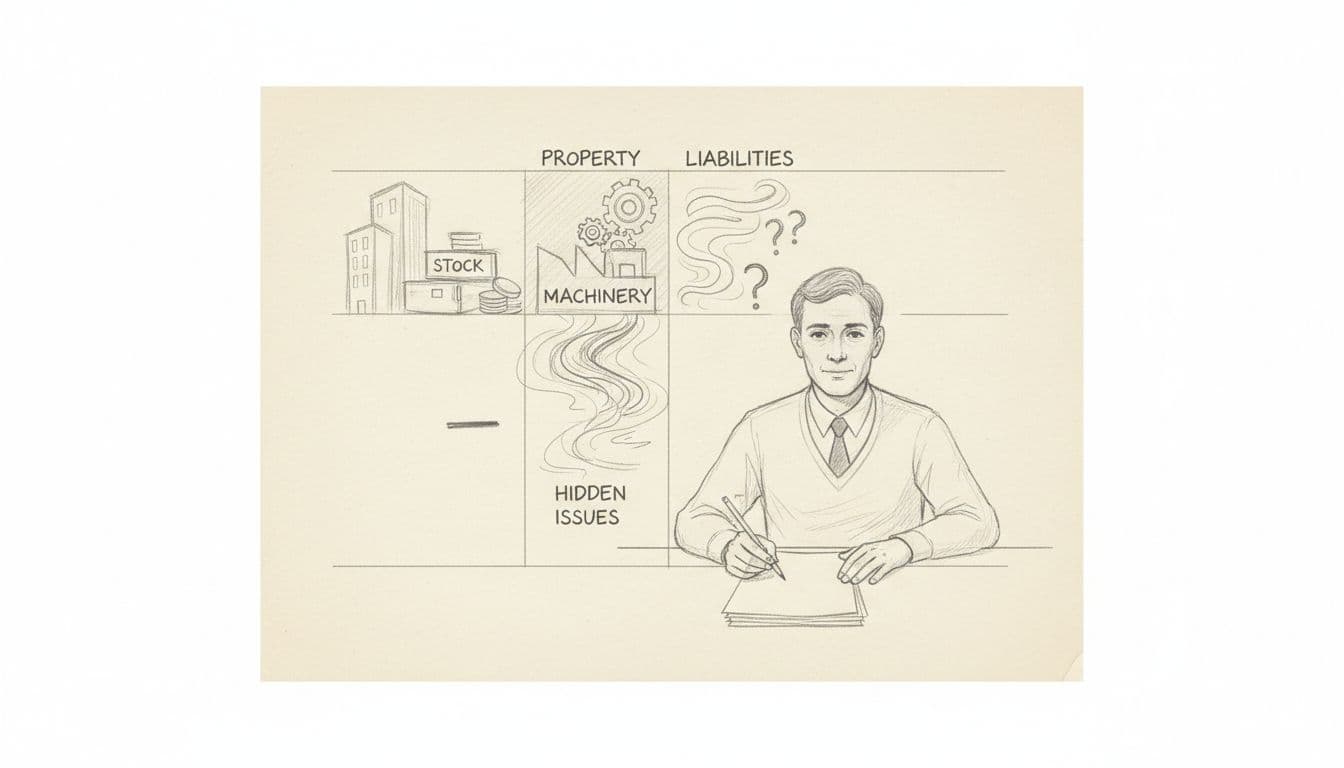

Asset-based valuation for asset-heavy or weak-performing companies

Sometimes profits are not the right place to start. If the business is property-rich, machinery-heavy, or underperforming, net assets or adjusted balance sheet value may matter more than earnings.

This is common where a company owns valuable fixed assets, holds significant stock, or has limited trading strength. It is also relevant where the business is loss-making, has volatile earnings, or may be closer to an orderly wind-down than a continuing trade.

The basic approach is to take the assets, then deduct liabilities. In practice, that is rarely the end of the story. Some assets need to be restated at real value, not book value, and hidden liabilities often sit beneath the surface.

A proper review usually looks at:

- Old stock that may be overvalued or obsolete.

- Fixed assets that need a market-based assessment rather than balance sheet values.

- Debtors that may not be fully recoverable.

- Hidden liabilities such as tax exposures, lease obligations, or warranty claims.

This method is often more suitable for companies where the balance sheet tells a better story than the profit and loss account. It is also a useful cross-check where a trading valuation seems too high or too low.

For shareholder disputes, that matters. A company can look profitable on paper and still have weak underlying assets, or it can look thin on profits while holding real value in property or equipment. The valuation has to catch that difference.

A good valuer will usually test the balance sheet carefully, then decide whether the asset base should lead the valuation or sit alongside an earnings-based check. That is the sort of judgement that keeps the numbers grounded and defensible.

The key adjustments that can make or break the final figure

This is where shareholder dispute valuations often win or lose credibility. The headline profit or balance sheet figure rarely tells the full story, because small adjustments can move the result by a lot.

The job is not to massage the numbers. It is to strip out distortions, check the true economic position, and arrive at a figure that reflects what the business actually earns, what it actually owes, and what a shareholder is actually entitled to receive.

Normalising profits so the numbers reflect the real business

A clean valuation starts with clean earnings. If the accounts include unusual costs, inflated director pay, private spending, or one-off income, the profit figure can mislead both sides.

That is why normalising adjustments matter. You remove items that do not belong in the ongoing trade, then add back anything the company has absorbed that a buyer would not expect to repeat. The aim is simple, find the business’s true earning power.

Common adjustments include:

- Unusual costs such as legal disputes, restructuring charges, or exceptional repair bills.

- Director pay that is above market rate, especially where the owner works in the business.

- Personal expenses run through the company, such as private travel, family use, or lifestyle costs.

- One-off income that flatters a single year but will not come back.

A director taking a large salary can distort profit just as much as private spending hidden in overheads. The same applies to a windfall sale, compensation payment, or insurance receipt. If you leave those items in place, the valuation can drift away from reality very quickly.

The question is not what the accounts say after the dust has settled. The question is what the business would earn on a normal trading day, under normal trading terms.

That is why careful normalisation is not a technical side issue. It is often the difference between a fair price and a figure that one side will challenge straight away.

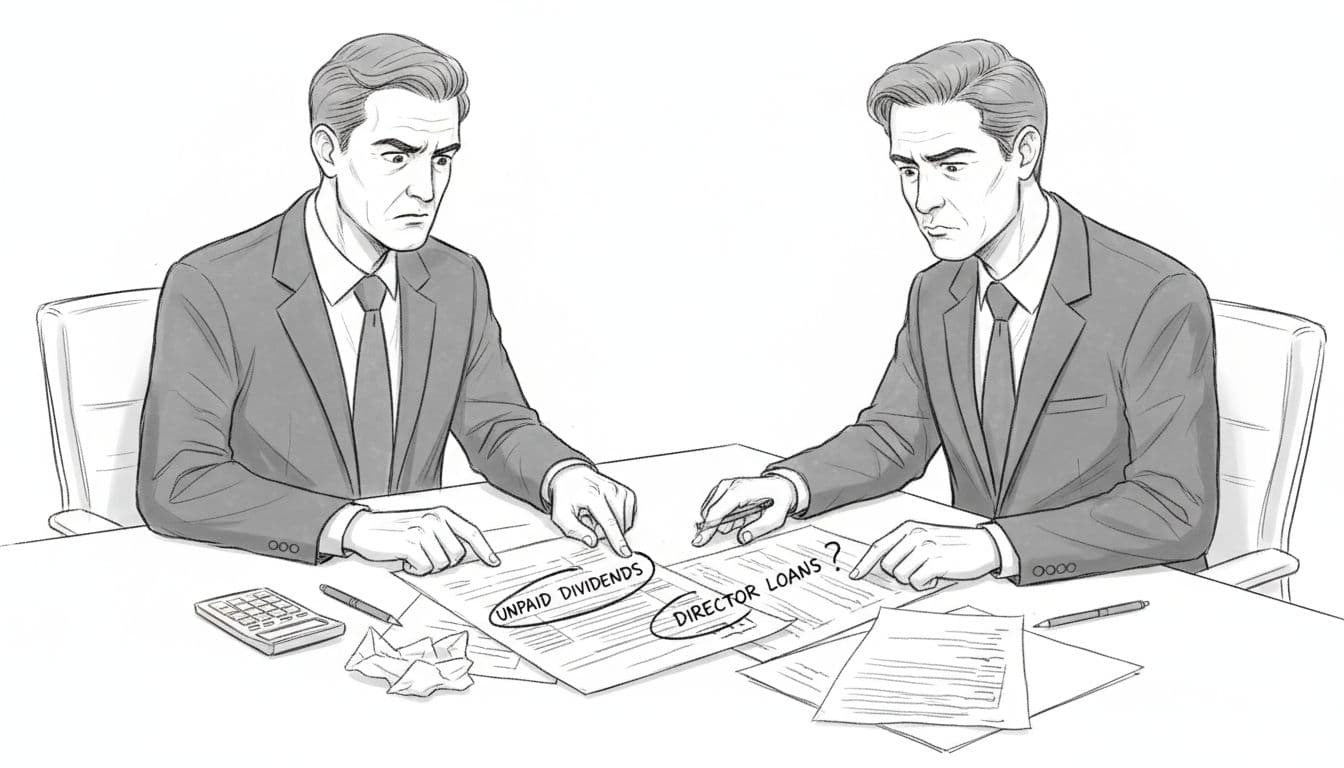

Handling unpaid dividends, loans, and director drawings

These balances often sit at the heart of the fight. They can change the final share price, but they can also change what a shareholder is actually owed once the dust settles.

Unpaid dividends may be treated as a debt due to the shareholder, depending on how they were declared and recorded. Director loans may need to be repaid to the company, or offset against what the shareholder is claiming. Director drawings can be even messier, because they often blur the line between salary, drawings, loan account movements, and informal withdrawals.

That is why these items need a proper check. A balance sheet can look tidy on the surface while hiding a real claim, or a real liability, underneath it.

The main pressure points are usually these:

- Unpaid dividends may support a higher settlement figure if they were validly declared and remain outstanding.

- Director loan accounts can reduce what a shareholder receives if money has been taken out and not repaid.

- Drawings can create arguments over whether sums were remuneration, repayment, or an overdrawn balance.

- Offsets and cross-claims often matter, because one shareholder’s claim may be matched by another amount owed back to the company.

This is where disputes get sticky. One side sees money that should have been paid. The other sees a debt that should come back first. Both are looking at the same ledger, but they are not reading the same outcome.

A proper valuation has to check the legal and accounting treatment, then separate what is genuinely distributable from what is simply being argued over. Miss that step, and the share price can be wrong in either direction.

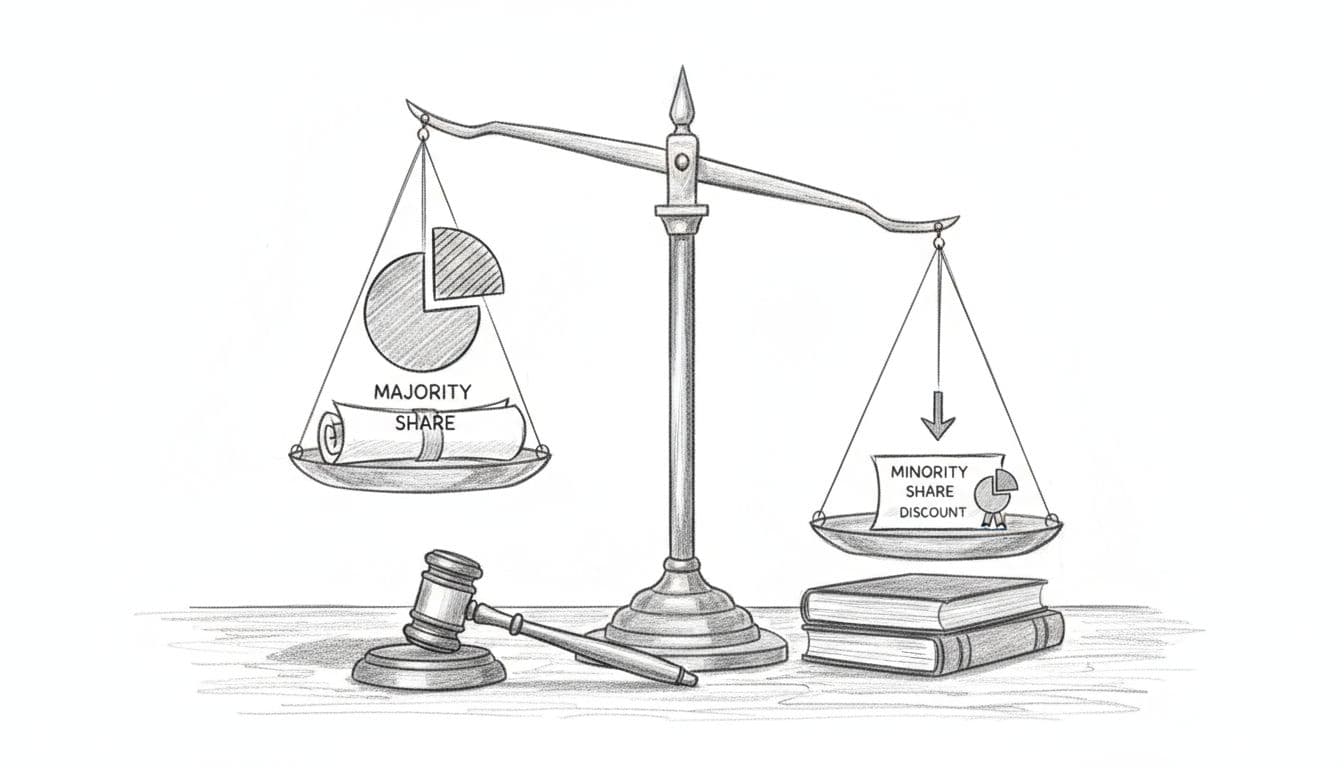

Why minority discounts are often disputed

A minority discount is a reduction in value because a small shareholding usually carries less control and is harder to sell. In a normal open market sale, that logic can make sense. In a shareholder dispute, it is often the first thing both sides argue about.

Why? Because a forced sale is not the same as a willing sale. The shareholder is not shopping the stake around the market. They are usually being bought out in difficult circumstances, often after exclusion, deadlock, or unfair prejudice. That changes the fairness question.

The dispute usually centres on whether the stake should be valued as:

- a minority interest, with a discount for lack of control or marketability, or

- a proportionate share of the whole company, without any discount applied.

There is no automatic answer. The right treatment depends on the facts, the shareholder agreements, the articles, the behaviour of the parties, and the legal context of the claim. Courts are wary of rewarding wrongdoing, but they also avoid a one-size-fits-all rule.

For that reason, minority discounts are rarely just a maths issue. They are a fairness issue. If one shareholder has been pushed out, denied information, or stripped of influence, a discount can look like a second punishment layered on top of the first.

That is why the valuation has to be defended properly. The adjustment may be valid, it may be reduced, or it may be rejected altogether. What matters is the reasoning behind it, not just the percentage on the page.

How a strong valuation report stands up in a dispute

A valuation report in a shareholder dispute has one job, it has to hold its shape when pressure goes on. If the other side challenges the assumptions, the method, or the numbers, a weak report folds quickly. A strong one stays clear, evidence-led, and credible.

That is why the quality of the report matters as much as the headline figure. In a dispute, the question is rarely just “what is the business worth?” It is, “can this figure survive scrutiny from solicitors, accountants, and the court?”

Why independence and experience matter

An independent Chartered Accountant carries more weight than someone close to the company because the valuation has to look unbiased, not convenient. If the valuer is tied to management, the report can look like an argument in disguise. That weakens credibility fast.

Experience matters just as much. A dispute valuation is not a routine year-end exercise. It needs judgement, commercial awareness, and the ability to defend the numbers under questioning, which is where specialist dispute experience becomes a real advantage.

A partner-led process also helps. At Consult EFC, the work is handled at partner level, which keeps the process focused, confidential, and consistent from start to finish. That matters when the stakes are high and the facts are sensitive.

In practice, the difference is simple:

- Independence gives the report credibility.

- Dispute experience gives it resilience.

- Partner-led delivery keeps the work tight, private, and controlled.

A valuation report is only as strong as the person prepared to defend it.

What a court-ready report should include

A court-ready report does not need fancy language. It needs the right components, set out clearly and supported properly. If you are checking whether a report is complete, this is the place to start.

A solid report should normally include:

- The valuation basis

State whether the report is based on fair value, market value, or another basis. In a shareholder dispute, that distinction matters. - The method used

Explain whether the value comes from earnings, discounted cash flow, net assets, or a combination. The reader should understand why that method fits the business. - Key assumptions

Set out the assumptions behind growth, margins, discount rates, multiples, and normalised earnings. If a figure depends on an assumption, say so plainly. - Supporting evidence

Back up the analysis with management accounts, filed accounts, tax returns, bank data, contracts, and other relevant records. A report without evidence is just opinion. - Limits and risks

Be clear about any missing records, unresolved disputes, or areas where the numbers are less certain. A strong report does not pretend every input is perfect.

The best reports are not overcomplicated. They are readable, structured, and honest about what has been tested and what has not. That makes them easier to use in negotiation and much harder to pick apart later.

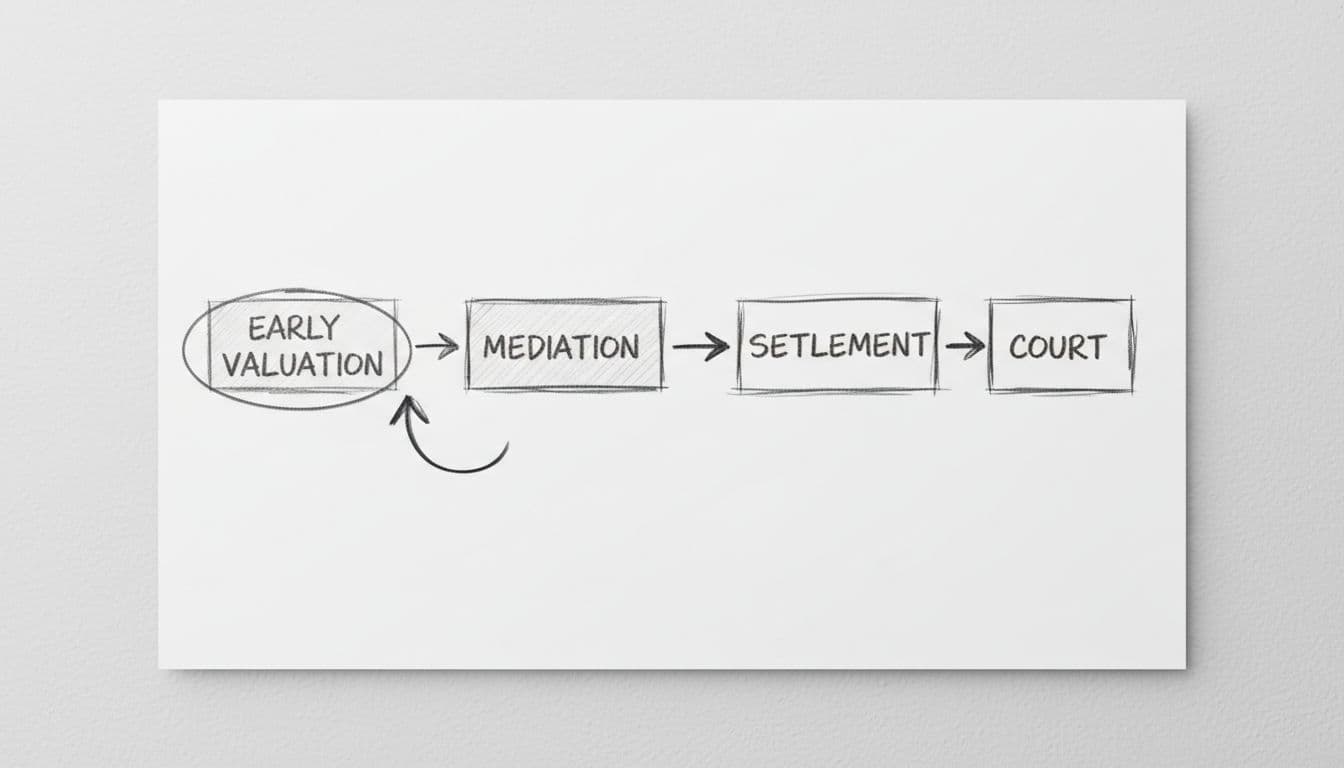

When to get a valuation done in the dispute process

Timing can change the outcome. If you get a valuation done early, you give yourself a proper starting point for settlement talks, mediation, and planning the next move. You stop arguing in the abstract and start dealing with a real number.

That early clarity can save time and money. It may expose a wide gap, but it can also show when the gap is narrower than expected. Either way, it gives everyone a better basis for decision-making.

Waiting too long usually makes things worse. Costs rise, positions harden, records disappear, and the dispute becomes more expensive to unwind. By then, the valuation is not just about price, it is about repairing the damage caused by delay.

Early valuation is especially useful when you are:

- Considering settlement, because it gives you a number to work with.

- Heading into mediation, because it keeps the discussion grounded.

- Planning a buyout or exit, because it shows what is realistic.

- Assessing litigation risk, because it highlights weak assumptions before they become a problem.

A valuation done at the right time can act like a pressure valve. It does not solve the dispute on its own, but it gives the parties something concrete to negotiate against. That is often the difference between a managed resolution and a costly stalemate.

How SMEs can prepare before asking for a valuation

A valuation is only as strong as the information behind it. If the records are incomplete, the discussion slows down, the costs rise, and the final figure becomes easier to challenge.

For SMEs in a shareholder dispute, preparation is not about tidying a file cabinet. It is about giving the valuer a clean evidential base, so the report can stand up to scrutiny and support a fair outcome. That is the difference between a figure that moves the dispute forward and one that creates more argument.

The documents and records that matter most

Start with the basics, then build out the picture. A good valuer needs to see both the formal records and the background to the dispute, because value is shaped by numbers, ownership, and behaviour.

The core pack should include:

- Accounts and management figures for the last few years, including draft or monthly management accounts where available.

- Bank statements so cash movement, unusual payments, and director withdrawals can be checked properly.

- Shareholder agreements and articles of association to show rights, restrictions, and any buyout wording.

- Dividend history to confirm what was declared, what was paid, and whether anything remains unpaid.

- Payroll records to separate salary, bonuses, and drawings.

- Loan balances for director loan accounts, inter-company balances, and any money owed by or to shareholders.

- Emails and minutes that show how the dispute started, when trust broke down, and what decisions were taken.

That last point matters more than many owners realise. A short email trail or board minute can explain why one side stopped receiving information, why dividends were withheld, or why the business moved from disagreement to deadlock.

If the facts behind the dispute are missing, the valuation has to work harder. That usually means more time, more cost, and more room for challenge.

The cleanest files are not always perfect, but they are traceable. A valuer can work with gaps if the pattern is clear. What slows everything down is a business that has to reconstruct its own history from memory.

Common mistakes that slow the process down

The biggest delays usually come from avoidable problems. Poor preparation does not just create admin. It weakens the valuation, because the numbers become harder to trust.

The most common mistakes are straightforward:

- Poor record keeping

Missing accounts, old bank statements, and incomplete management figures make it harder to test profit, cash flow, and liabilities. If the trail is broken, the valuation becomes more expensive to evidence. - Mixed personal and business खर्च

Personal spending run through the company blurs the true trading result. It also creates arguments over what should be added back, what should be removed, and whether the books can be trusted at all. - Unclear ownership

Informal share transfers, weak cap table records, and missing loan paperwork create doubt over who owns what. That is a serious issue in a shareholder dispute, because ownership affects value and settlement leverage. - Waiting until the dispute is emotional

Once the rows get personal, people stop sharing information and start protecting positions. At that stage, records go missing, explanations become selective, and every assumption costs more to test.

The result is predictable. The valuer has to spend more time untangling the business, which increases fees and can leave both sides with a weaker position. A clean file does not remove the dispute, but it gives the valuation a firmer foundation.

The right move is to prepare early, gather the records properly, and present the facts before the argument takes over. That is where Consult EFC adds real value, because a disciplined valuation process starts with disciplined information.

Conclusion

Valuing a business for shareholder disputes is not a box-ticking exercise. The right figure has to be fair, independent, and grounded in proper evidence, or it will fall apart the moment the other side tests it.

That is why the best valuations do more than set a price. They help settle the matter sooner, protect value, and reduce stress for everyone caught in the dispute. Get the valuation wrong, and the disagreement drags on. Get it right, and the conversation becomes much easier to resolve.

If you need trusted SME valuation support, Consult EFC can help with a clear, defensible approach that is built for real shareholder disputes, not guesswork.

Not sure what your business is worth right now?

Request a confidential valuation — ICAEW Chartered Accountants, Big Four trained. No junior analysts. Fixed fees.

Request My Valuation

Over 12 years across Big Four audit, Investment Banking and corporate advisory. Kishen works with UK SMEs on valuations, exit planning, fundraising and financial strategy. ICAEW regulated. Big Four trained. Based in London.