A SSAS deal can look simple on paper. Buy the shares, make the loan, sign the transfer. But if the valuation is weak, the whole transaction can start to wobble.

For trustees, a SSAS business valuation is not a box-ticking exercise. It is part of the evidence that shows a deal is fair, commercial, and properly documented. The rules can feel technical, but the aim is plain enough, protect the scheme and avoid expensive mistakes.

Why a SSAS business valuation matters for trustees

Trustees are there to act for the pension scheme, not to back an optimistic number because it suits the business. That is why valuation evidence matters. It supports decisions on buying shares, lending to a connected company, or investing in a business linked to the members.

HMRC expects an open market view. Not a hopeful internal estimate. Not a round number agreed over coffee. If the transaction is ever reviewed, trustees need to show how they reached the price or loan terms, and why those terms were right for the scheme.

How the valuation helps prove the deal is commercial

A proper valuation helps show the deal is being done at arm’s length. That means the scheme is not overpaying for shares, undercharging for risk, or accepting weak security.

For trustees, that matters in two ways. First, it supports fair pricing. Second, it supports the decision-making record, including trustee minutes, loan terms, and the commercial logic behind the transaction.

What can go wrong if trustees rely on guesswork

Guesswork creates weak ground. HMRC can challenge the transaction. Administrators or advisers may stop the deal until proper evidence is produced. Due diligence can stall if lenders, buyers, or auditors ask how the figure was set.

There is also a more basic problem. If the security does not back the loan, or the asset price is inflated, the scheme carries the loss. Trustees then have a poor defence because there is no independent valuation to point to.

The main situations where trustees usually need a valuation

The need for a valuation usually appears when the scheme and the business are closely linked. That is common in UK SMEs, where directors, shareholders, and trustees often overlap.

Lending SSAS funds to a connected company

A loan to a connected employer or related company has to be commercial. Trustees need evidence that the loan amount, interest rate, and security stack up. If the security is worth less than the loan, the scheme is exposed from day one.

Buying shares, a business, or other connected assets

When the seller, buyer, or company is linked to the scheme, market value matters even more. Trustees should not rely on a founder valuation or a historic fundraising price. An independent view helps support the purchase price and the rationale for the deal.

Supporting exits, investment rounds, or share transfers

A valuation can also help when trustees are planning a sale, a new investment round, or a share transfer. For growing SMEs, clean paperwork matters. It helps the transaction move faster and makes the story easier to defend later.

What HMRC and the pensions rules expect from trustees

There is no single SSAS valuation rulebook that answers every question. Trustees still have to meet wider pension and tax rules, and connected party transactions are looked at closely. Market value, proper process, and fair treatment are the themes that run through all of it.

Since the 2024/25 tax year, HMRC reporting has also become more detailed for SSAS arrangements. Investment information, fees, and scheme data are under closer review. That makes weak records harder to hide.

A valuation is not there to justify a deal you already want to do. It is there to test whether the deal should happen on those terms.

Why independence matters so much

If the person valuing the business is tied to the deal, the report carries less weight. Trustees need an independent opinion that is current, reasoned, and free from pressure. If questions come later, independence is one of the first things people look at.

Why connected parties need extra care

Connected parties include trustees, members, family members, and businesses they control. These are not banned relationships, but they do bring higher scrutiny. Trustees need to show the scheme is not giving favourable terms just because the other side is familiar.

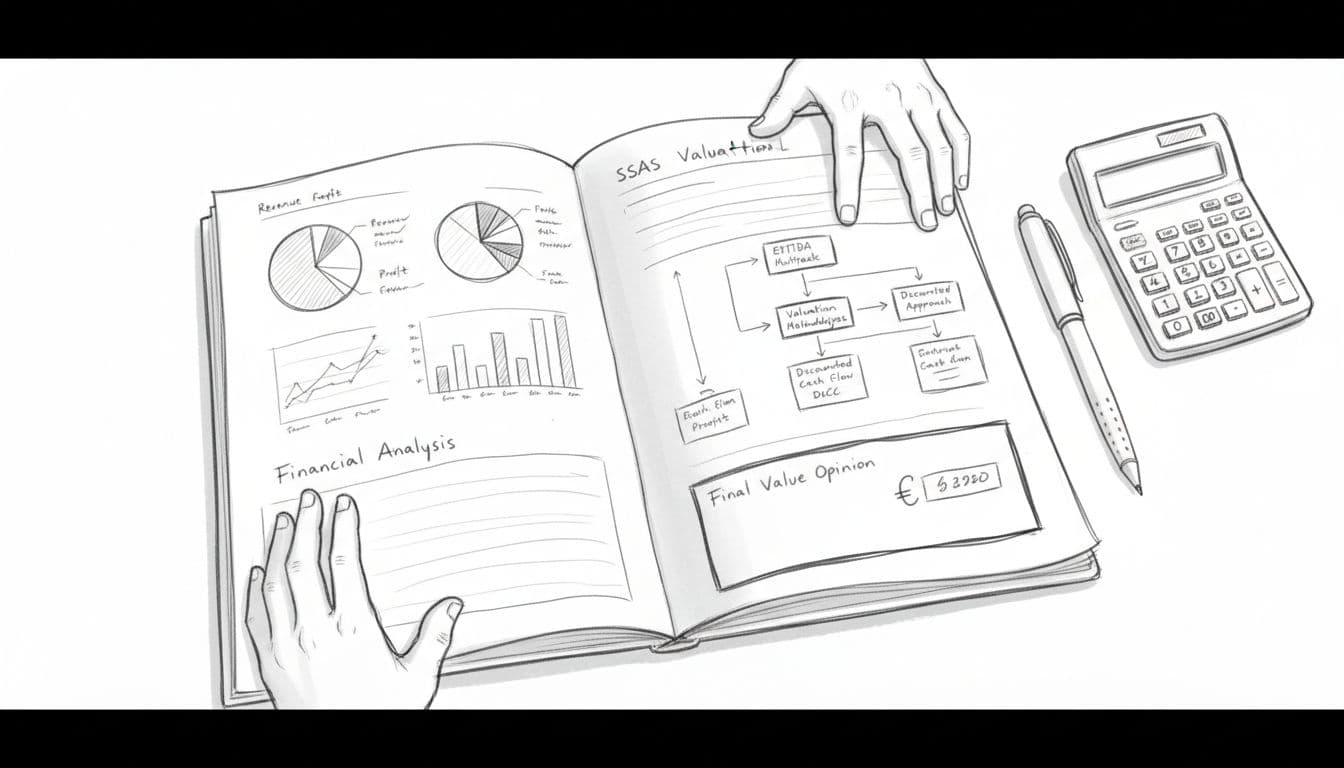

What a solid SSAS business valuation report should include

A serious report should do more than give one number. It should show the business facts, the method used, and the evidence behind the conclusion.

The business facts, financials, and assumptions used

Trustees should expect current accounts, management figures, trading history, share details, and any relevant contracts to be reviewed. Assumptions should be sensible and stated clearly. If the report cannot show how it got to the figure, it is not much use.

The valuation method and why it was chosen

Different businesses need different methods. EBITDA multiples may fit established trading companies. Discounted cash flow may suit forecast-led cases. Comparable transactions can help where market evidence exists. The report should explain why the chosen method fits the business and the transaction.

Clear opinion of value and supporting evidence

Trustees need a clear value conclusion, not pages of jargon with no answer. The report should also be detailed enough to stand up to HMRC, lenders, investors, or a buyer reviewing the file later.

How trustees can prepare before asking for a valuation

Good preparation saves time and avoids rework. It also improves the quality of the final report.

Gather the right company records early

Before instructing a valuer, pull together the basics:

- recent statutory accounts

- up-to-date management figures

- share capital details

- loan documents and security papers

- major customer or supplier contracts, where relevant

Clean records make the process faster and the opinion stronger.

Be clear about the purpose of the valuation

A valuation for a secured SSAS loan is not the same as one for an exit, a share transfer, or HMRC review. Purpose drives method, scope, and assumptions. Trustees should be clear about what decision the report needs to support.

Choose a valuer who understands SSAS work

This is a specialist job. Trustees need a chartered accountant who understands SME transactions, connected party issues, and what a defensible report looks like in practice.

How Consult EFC helps trustees meet valuation requirements properly

Consult EFC works with UK SMEs and trustees who need valuation evidence they can rely on. The focus is simple, partner-led, confidential, fixed-fee work that is suitable for due diligence and built for real transactions.

A partner-led approach with no junior hand-offs

That matters when the facts are messy, timelines are tight, or judgement is needed. Direct senior involvement means fewer gaps, better questions, and quicker decisions.

Reports built for HMRC, lenders, investors, and buyers

A report should work in the real world, not only on a spreadsheet. Consult EFC prepares valuations that are credible for compliance and practical for funding rounds, exits, share transfers, and connected business deals.

Conclusion

Trustees should not move first and ask valuation questions later. In a SSAS, proper evidence comes before the transaction, not after it.

A sound valuation supports compliance, cleaner decisions, and far less stress if the deal is reviewed. When the price, security, and reasoning are properly documented, the scheme is better protected and the business has a firmer platform for its next step.

Not sure what your business is worth right now?

Request a confidential valuation — ICAEW Chartered Accountants, Big Four trained. No junior analysts. Fixed fees.

Request My Valuation

Over 12 years across Big Four audit, Investment Banking and corporate advisory. Kishen works with UK SMEs on valuations, exit planning, fundraising and financial strategy. ICAEW regulated. Big Four trained. Based in London.